Let me be real with you — I’ve seen a hundred “cost of living” articles that just dump a table of numbers and call it a day. That’s not what this is.

If you’re seriously thinking about moving to Florida, or you’re trying to figure out whether the Sunshine State is still worth the hype in 2026, you need the full picture. The good, the not-so-great, and the stuff that catches people completely off guard when the first utility bill hits in August.

So let’s actually talk about it.

Why Florida Keeps Coming Up in the “Should I Move?” Conversation

Florida added over 300,000 new residents in 2023 alone. People are coming from California, New York, New Jersey, Illinois — places where the tax burden and housing costs have quietly become unbearable. But here’s the thing: Florida isn’t cheap anymore. It used to be. It’s not in 2026.

What it is, however, is relatively affordable compared to the states most people are fleeing from. And that relative value? That’s what we’re going to break down today.

The Big Number: Florida’s Cost of Living Index

According to the Missouri Economic Research and Information Center (MERIC), Florida sits at a cost of living index of around 103–105 — meaning it’s slightly above the national average of 100.

Compare that to:

- California: ~142

- New York: ~139

- Massachusetts: ~148

- Texas: ~92

- Tennessee: ~89

- North Carolina: ~96

So yes — Florida is cheaper than the coasts. But it’s not cheap in the way Texas or Tennessee is cheap. There’s nuance here, and the nuance matters depending on what category of expenses hits hardest for your lifestyle.

Housing: Where Florida Gets Complicated

This is the big one. And I want to be honest with you because a lot of content online glosses over how much housing has shifted.

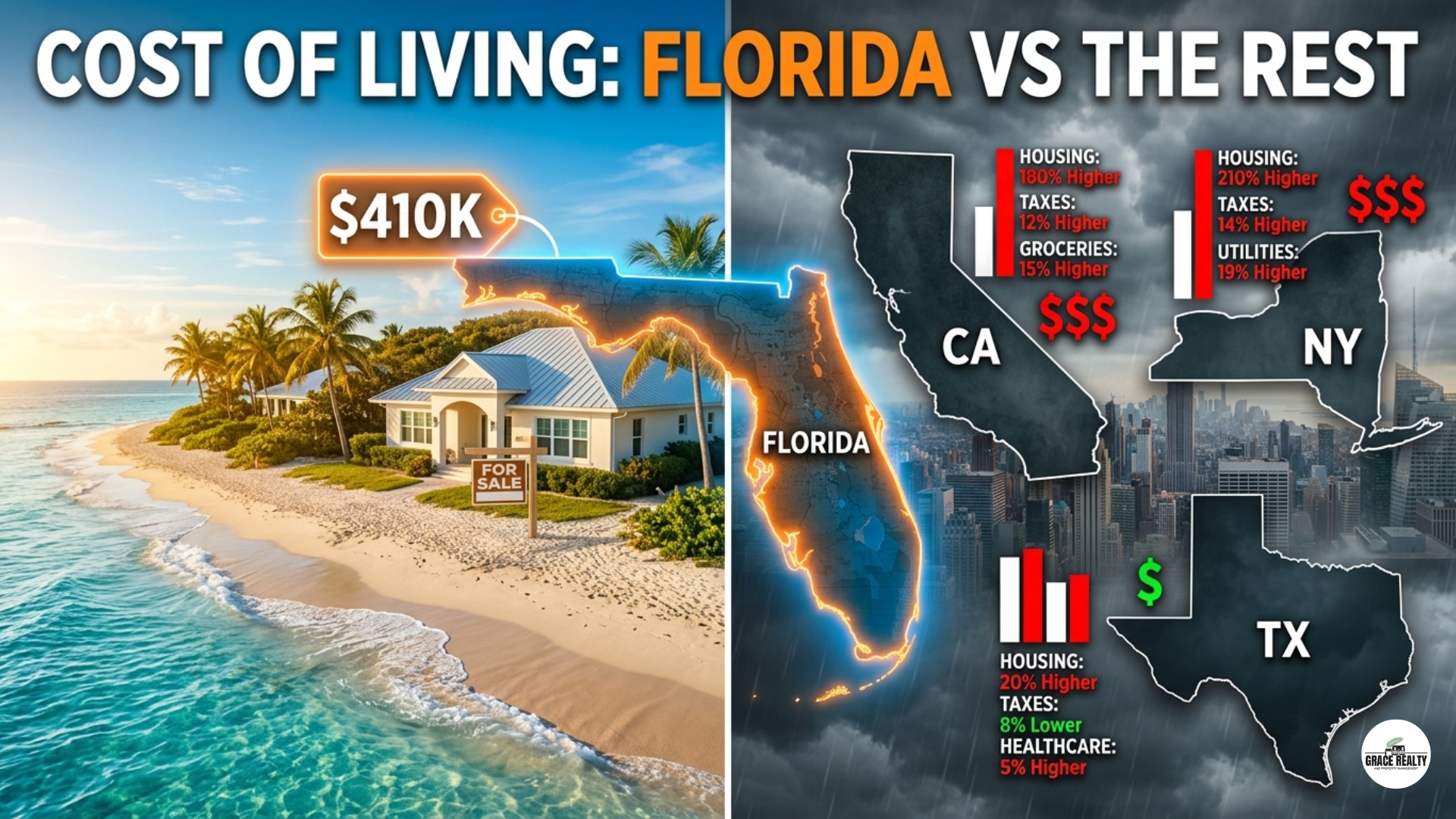

Florida median home price (2026): ~$410,000

That sounds rough, but look at the context:

- California median: ~$790,000

- New York (state): ~$450,000

- Texas median: ~$310,000

- Tennessee median: ~$330,000

- North Carolina median: ~$360,000

Florida is more expensive than the Sun Belt alternatives, but it’s still dramatically cheaper than the coasts. The real story, though, is where in Florida you’re looking.

Miami-Dade County? Median home prices are pushing $620,000+. Rent for a 2-bedroom? Easily $2,800–$3,500/month.

Tampa Bay Area? You’re looking at $380,000–$450,000 for a median home. Rent for a 2BR runs $2,000–$2,600.

Orlando suburbs? More manageable. Median around $350,000, with rent often in the $1,800–$2,400 range.

Jacksonville or Pensacola? Now we’re talking. Medians closer to $280,000–$320,000 with rents that can drop below $1,600/month.

The Florida housing conversation isn’t one-size-fits-all. It’s really a collection of different markets wearing the same state flag.

Taxes: This Is Where Florida Actually Wins

Okay — here’s where the Florida argument really holds up, and it’s genuinely significant.

Florida has no state income tax.

Zero. None. That’s not a small thing. If you’re moving from California, you were potentially paying 9.3%–13.3% of your income to the state. From New York, up to 10.9%. From New Jersey, up to 10.75%.

For someone earning $100,000/year, moving from California to Florida could mean keeping an extra $9,000–$13,000 annually — before you factor in anything else.

That single line item changes the entire cost-of-living math for middle and upper-middle earners.

Florida does have a 6% state sales tax, plus local surtaxes that bring it to 7%–8.5% depending on the county. That’s comparable to most states. Property taxes, however, are moderate — averaging around 0.83% effective rate, which is actually lower than Texas (1.6%+), New York (~1.4%), and Illinois (~2.2%).

Insurance: The Hidden Cost That’s Breaking Floridians’ Budgets

I would be doing you a disservice if I didn’t dedicate real space to this.

Homeowners insurance in Florida is a crisis right now.

The average annual homeowners insurance premium in Florida is approximately $3,600–$6,000 depending on location, age of home, and coverage level. That’s 2–4x the national average of around $1,400–$1,800.

Why? Hurricanes, flooding risk, a reinsurance market that’s been hammered by claims, and a legal environment that historically encouraged excessive litigation (though recent tort reform has started to help).

If you’re buying near the coast — Miami, Naples, Fort Myers, the Keys — your insurance premiums could easily run $8,000–$15,000+ per year. Some homeowners in high-risk zones are being dropped by insurers entirely and pushed to Florida’s insurer of last resort, Citizens Property Insurance.

This is the number that shocks people. Budget for it before you budget for anything else.

Groceries and Everyday Expenses

Grocery costs in Florida are close to the national average — typically 2–5% above the baseline due to transportation costs and tourism-driven pricing in certain areas.

- A gallon of milk: ~$3.80–$4.20

- Gas (statewide average, 2026): ~$3.30–$3.70/gallon

- A restaurant meal (mid-range): $15–$22 per person

Compare this to California where that same restaurant meal could run $22–$35, or New York where $25+ for a casual lunch is unremarkable.

Day-to-day spending in Florida, outside of housing and insurance, is pretty manageable.

Healthcare Costs in Florida vs Other States

Healthcare is one area where Florida performs middling to average. The state has a solid concentration of healthcare providers, especially in major metros, but costs can vary.

Average health insurance premium (individual, ACA marketplace, 2026): $480–$560/month — roughly in line with national averages.

Florida does rank lower than California and New York in out-of-pocket costs but higher than states like Tennessee or Georgia for certain coverage types.

Utilities: Prepare for Air Conditioning

Here’s a seasonal reality check. Florida summers are brutal — not just hot, but humid in a way that makes air conditioning non-negotiable from May through October.

Average monthly utility bill in Florida: $160–$220/month

Peak summer months (July–September)? Some households see $300–$400/month electricity bills. This is higher than most non-Southern states, and it’s a cost that new Floridians often underestimate dramatically.

Compare to:

- Texas: similar, sometimes higher in extreme heat years

- California: $130–$180/month (milder climate)

- New York: $130–$170/month but with higher heating costs in winter

Florida vs Texas: The Most Common Comparison

People constantly debate this one, so let’s settle it directly.

| Category | Florida | Texas |

|---|---|---|

| State Income Tax | None | None |

| Median Home Price | ~$410K | ~$310K |

| Avg. Property Tax Rate | ~0.83% | ~1.60% |

| Homeowners Insurance | $3,600–$6,000/yr | $2,000–$3,500/yr |

| COL Index | ~103–105 | ~92 |

| Sales Tax | 6–8.5% | 6.25–8.25% |

The honest answer: Texas is cheaper on paper, primarily because of lower home prices and lower property insurance. Florida wins on weather (no ice storms), beaches, and arguably lifestyle quality for certain demographics. If pure cost optimization is your goal, Texas edges it out. If you’re weighing livability alongside affordability, Florida stays competitive.

Florida vs California: The Most Obvious Win

If you’re coming from California, Florida will almost certainly feel like a financial relief — even with the insurance situation.

| Category | Florida | California |

|---|---|---|

| State Income Tax | 0% | 1–13.3% |

| Median Home Price | ~$410K | ~$790K |

| Avg. Rent (2BR) | $1,800–$2,800 | $2,500–$3,800 |

| COL Index | ~103–105 | ~142 |

| Gas (avg) | $3.40/gal | $4.60/gal |

On a $120,000 salary, a California resident could be paying $11,000–$14,000 in state income tax. In Florida: $0. That alone covers a substantial chunk of any higher insurance premiums.

Who Should Move to Florida? (And Who Shouldn’t)

Florida makes financial sense if you:

- Are fleeing a high-income-tax state (CA, NY, NJ, IL)

- Are retired or on investment income (no state tax on dividends, capital gains, Social Security)

- Can work remotely and want to skip the most expensive Florida metro areas

- Are buying inland or in secondary markets like Jacksonville, Ocala, or Gainesville

Florida might disappoint you financially if you:

- Are buying in South Florida on a moderate income

- Have an older home near the coast (insurance will hurt)

- Are comparing to true low-cost states like Tennessee, Mississippi, or Arkansas

- Are counting on Florida’s “cheap” reputation without checking 2026 numbers

The Bottom Line

Florida is not the bargain it was in 2015. But it’s still a legitimate financial upgrade for people escaping the highest-cost states in the country.

The income tax savings are real. The housing — depending on where you settle — can still be reasonable. The lifestyle is genuinely excellent for outdoor living, warm weather lovers, and retirees. But insurance costs are the wildcard, and they’re not going down anytime soon.

If you’re doing the math: run your specific numbers, factor in insurance aggressively, and compare your target Florida city to your origin state — not Florida as a vague abstraction.

The Sunshine State still makes sense for millions of people. Just go in with your eyes open.